An estimate, a quotation, and an invoice are three different documents used at three different stages of a sale. An estimate is an approximate, non-binding figure given early, when the full scope is not yet clear. A quotation is a fixed, itemised price the client can formally accept, given once the scope is known. An invoice is the final request for payment, issued after the goods or services have been delivered. The order is always estimate, then quotation, then invoice.

These three words are often used as if they mean the same thing, but treating a binding quote like a loose estimate, or sending an invoice before agreeing a price, is how businesses end up in payment disputes. Here is what separates them and when to use each.

What is an estimate?

An estimate is an educated guess at the cost of a job before the details are settled. It is useful early in a conversation, when a client asks "roughly how much would this cost?" and you do not yet know the full scope. An estimate is not binding, uses approximate figures or a range, and can move up or down as the work is defined. Because it is provisional, always label it clearly as an estimate so the client does not treat it as a firm price.

What is a quotation?

A quotation, or quote, is a fixed price for a defined job. Once you understand exactly what the client needs, you list the items, set the prices, and state a total the client can accept. A quotation is more formal than an estimate and is generally treated as binding for a stated validity period, for example thirty days. When the client accepts, that agreed price becomes the basis for the work and, later, the invoice.

What is an invoice?

An invoice is the request for payment, issued after the work is done or the goods are delivered. It restates the agreed items and prices, adds tax, shows the total due, and sets a payment deadline. The invoice is what creates the client's obligation to pay. Unlike an estimate or a quote, it is a financial record that belongs in your accounts and the client's.

The key differences at a glance

| Estimate | Quotation | Invoice | |

|---|---|---|---|

| When it is used | Before scope is set | Once scope is agreed | After work is delivered |

| Price | Approximate, can change | Fixed, itemised | Final amount due |

| Binding | No | Usually yes, for a set period | Yes, it demands payment |

| Purpose | Give a rough idea | Win the job at a set price | Get paid |

What order do you use them in?

The natural sequence is estimate, then quotation, then invoice. A client asks for a rough figure, so you send an estimate. They like the direction, you scope the job, and you send a quotation with a firm price. They accept, you do the work, and you send an invoice. Not every job needs all three. Small, well-defined jobs often skip the estimate and go straight to a quote, and repeat work may go straight to an invoice.

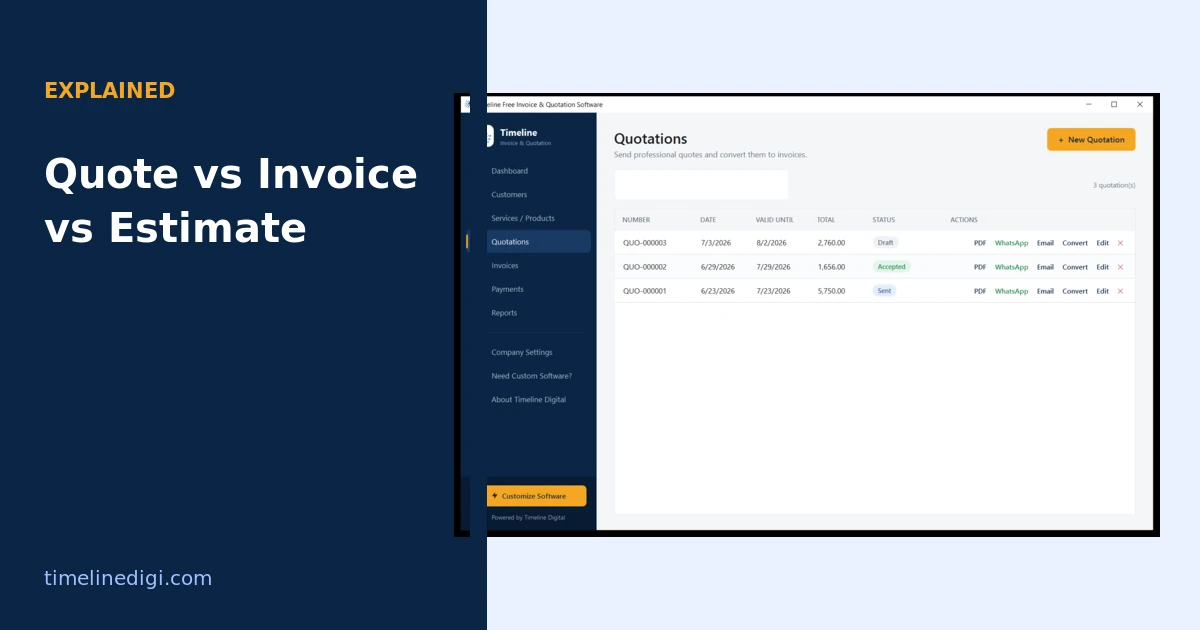

How to convert a quotation into an invoice

The cleanest workflow keeps quotes and invoices in one place so accepting a quote flows straight into billing. Good invoice software lets you convert an accepted quotation into an invoice in one click, carrying over the line items, prices, taxes, and terms, so nothing is retyped and nothing is billed twice. Timeline Invoice is free quotation and invoice software that does this: you send a quote, and when the client says yes, you convert it to an invoice instantly, with the quotation marked as converted.

Keeping the two connected is not just convenient. It prevents the classic mistakes of quoting one price and invoicing another, or forgetting to bill an accepted quote at all. If you are setting up your billing from scratch, start with how to create an invoice and what to include on an invoice.