Whether you sell generators in Lagos, boda-boda motorcycles in Nakuru, or fridges in Kumasi, the business model is the same: the customer pays a deposit, takes the goods (or takes them after finishing, if you run it layaway-style — both work), and pays small-small until the balance clears. Kenyans call it lipa mdogo mdogo — pay little by little. What kills the model isn't customers; it's poor records. This page shows how to fix that for free, with examples in naira, shillings and cedis.

Who is this hire purchase software for?

Timeline Free Installment Manager (v1.6.0, by Timeline Digital) fits dealers who finance their own sales:

- Electronics shops — phones, TVs, sound systems, solar kits, generators

- Furniture and appliance dealers — beds, sofas, fridges, freezers, cookers

- Motorcycle dealers — okada in Nigeria, boda-boda in Kenya and Uganda, sold on weekly plans to riders

- General traders running lipa mdogo mdogo for regular customers

Pick your country in the 2-step setup — Nigeria, Kenya, Ghana or 150+ others — and the whole app switches to ₦, KSh or ₵ automatically. Changing country later in Settings updates everything, and date formats are selectable.

How does a lipa mdogo mdogo plan look in the software? (Three examples)

| Nigeria (okada) | Kenya (boda-boda) | Ghana (fridge) | |

|---|---|---|---|

| Item | Motorcycle | Motorcycle | Double-door fridge |

| Total agreed price | ₦1,400,000 | KSh 180,000 | ₵9,000 |

| Deposit (down payment) | ₦400,000 | KSh 50,000 | ₵2,500 |

| Balance | ₦1,000,000 | KSh 130,000 | ₵6,500 |

| Installment | ₦50,000 weekly × 20 | KSh 5,000 weekly × 26 | ₵650 monthly × 10 |

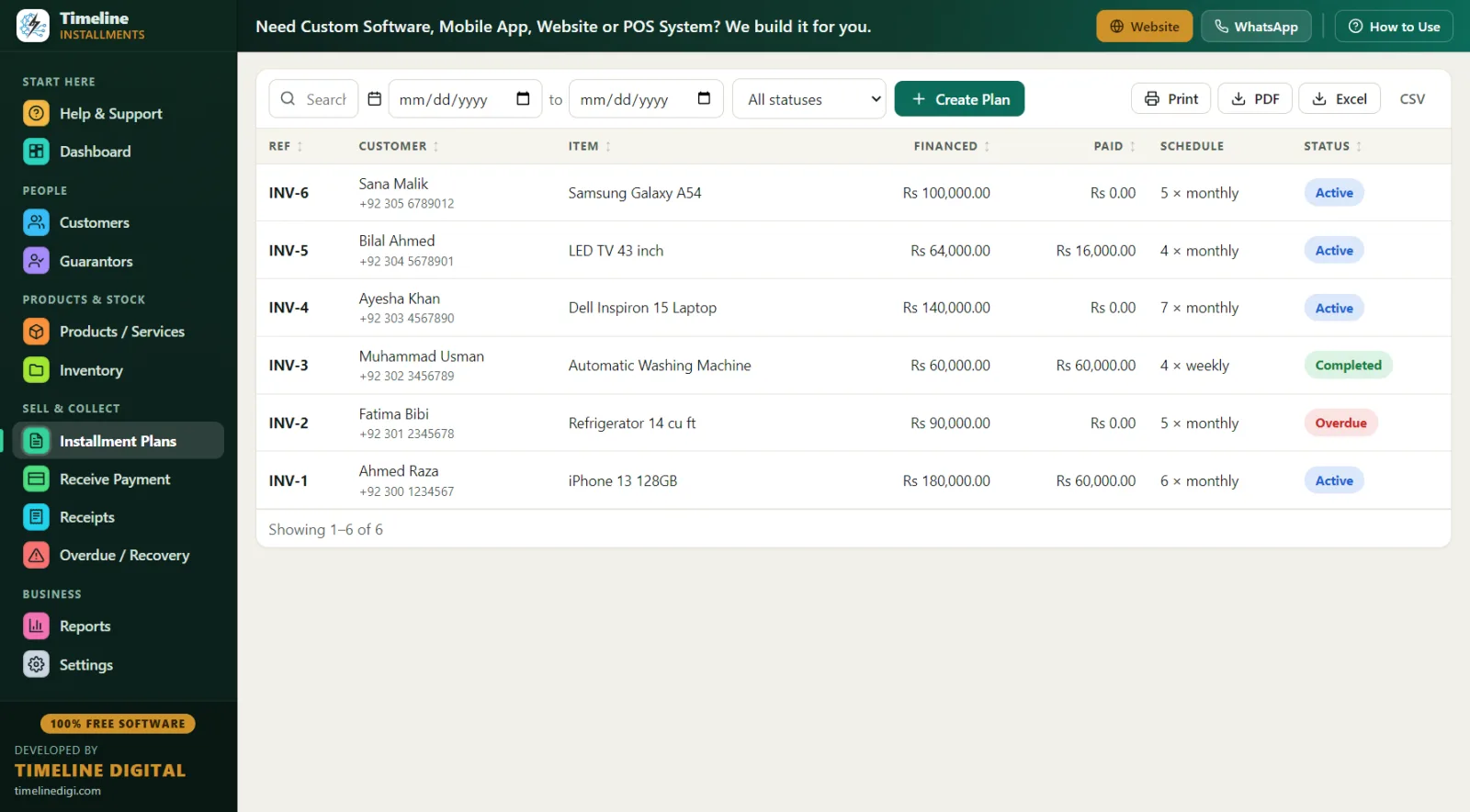

Creating any of these takes about three minutes: type-to-search the product, click "New Customer" to create the customer and plan together in one save, choose daily, weekly or monthly frequency, and check the live schedule preview so the customer sees every due date before signing. The deposit is automatically recorded as the first payment with a printed receipt, the plan gets a reference like INV-1, and stock reduces by one for tracked products.

There is no interest engine — you set the total hire purchase price yourself and the software splits and tracks it. Daily plans work too, which matters for okada and boda-boda riders who earn daily: ₦8,000 a day or KSh 800 a day is a plan the software handles natively.

How do guarantors work? (Built for how Africa actually does credit)

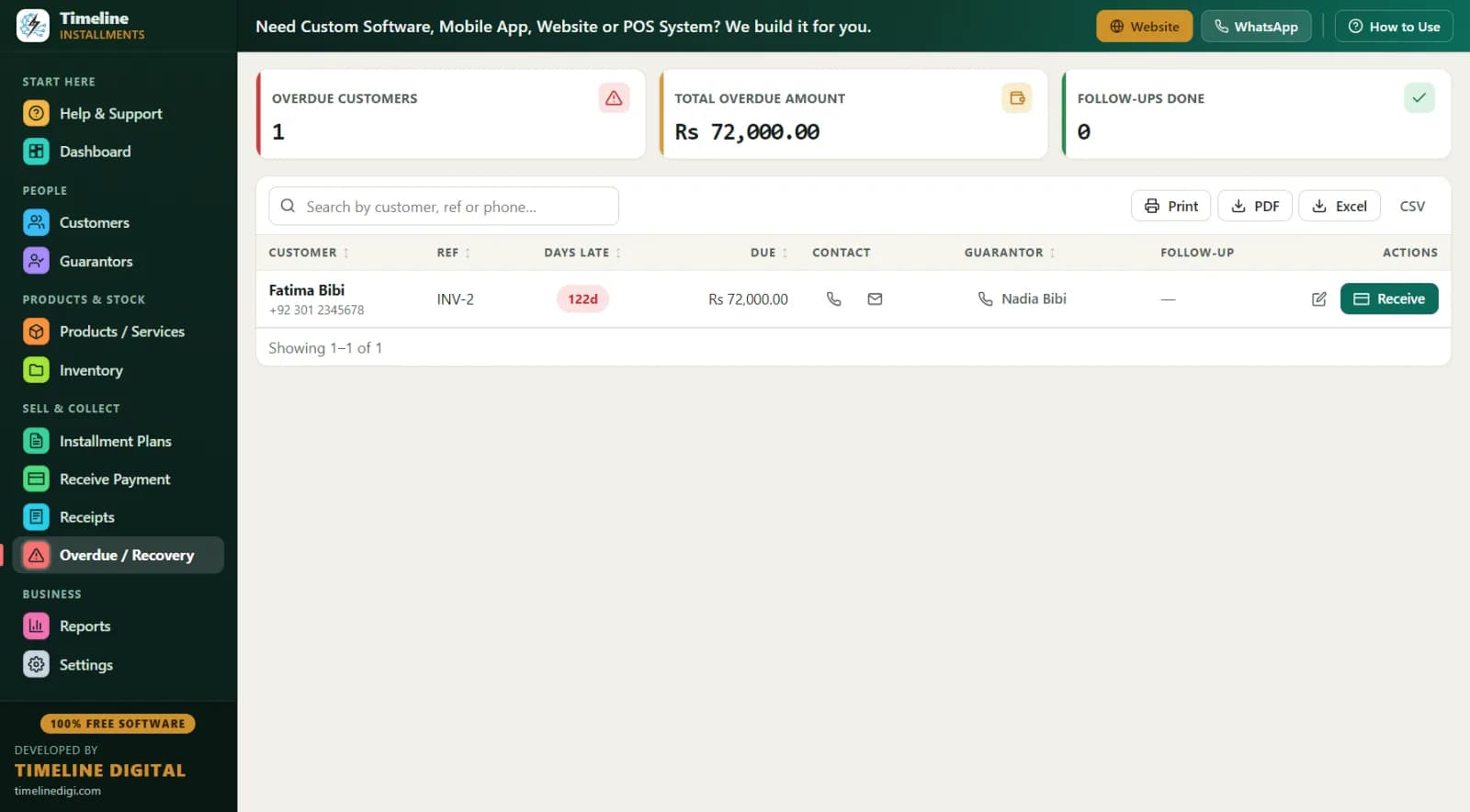

Across Nigeria, Kenya and Ghana, nobody sensible sells a motorcycle on credit without a guarantor — often two. The software treats guarantors as first-class records: each guarantor is linked to a specific customer and a specific plan, with name, relation, phone number and ID. When a rider stops answering his phone, the Overdue screen puts the guarantor's contact right next to the debt — days late, amount owed, customer phone, guarantor phone, and a notes field for your follow-up trail ("called chairman of the riders' association, promised Friday").

For the ID field, use whatever your market runs on: National ID (NIN in Nigeria, Huduma/National ID in Kenya, Ghana Card in Ghana), passport, or a driver's licence number. Name and phone are the only required fields; city and address complete the picture — and feed the Area Wise report, which shows receivables by town or area so collection trips are planned, not guessed.

How do I record M-Pesa and mobile money payments?

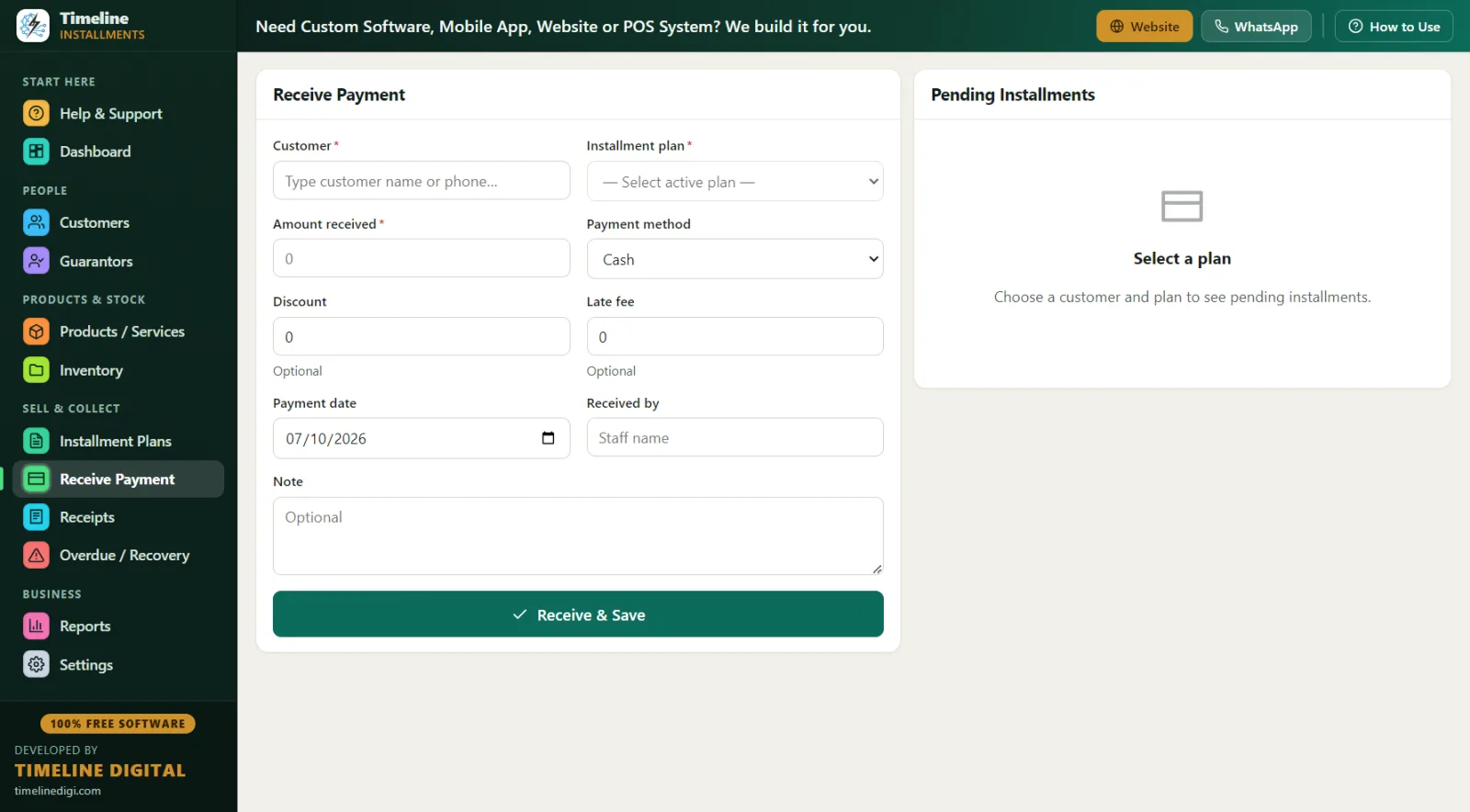

Most collections in Kenya arrive by M-Pesa; in Ghana it's momo; in Nigeria, bank transfer apps. The software records payment methods as cash, bank, card, online or other — record M-Pesa and momo payments under "online" (or "other" if you prefer to keep "online" for something else) and type the transaction code into the notes. Every payment gets an RCP-1 style receipt you can print or PDF, showing the amount in large print, "Installments Paid X of Y", and the remaining balance.

Partial payments are normal in lipa mdogo mdogo, and the software expects them: a rider who sends KSh 3,000 against a KSh 5,000 week has it applied oldest-first automatically, with the shortfall visible. Discounts for early settlement count toward closing the plan.

Why offline-first matters here

Timeline Free Installment Manager keeps its whole database on your shop PC. Nothing is uploaded, no server, no login — so when the network drops, when data bundles run out, when NEPA takes the light and you're on generator or inverter, your records still open instantly. A cloud system that needs a stable connection is a system that fails on exactly the days you're busiest. Offline-first means the software in a Lagos market stall works exactly like it would on fibre in an office tower.

The flip side of local data is that backups are on you — and they're one click. The software reminds you; keep a copy on a flash drive away from the shop, and a stolen or burnt PC costs you a machine, not your receivables book.

A day in the life of a boda-boda dealer in Nakuru

7:30 am — Open up. Dashboard shows today's expected collections; print the Daily Collection list. Twelve riders due today.

8:00 am–11:00 am — M-Pesa messages arrive as riders finish their morning runs. Each one: open Receive Payment, amount auto-fills, record under "online" with the M-Pesa code in notes, receipt saved as PDF.

12:30 pm — New sale: KSh 180,000 motorcycle, KSh 50,000 deposit, KSh 5,000 weekly for 26 weeks. Rider's brother and his stage chairman both recorded as guarantors with phones and IDs. Deposit receipted, schedule printed for the rider.

3:00 pm — Overdue review: four riders behind. Two paid after a call; one guarantor contacted; one flagged for a visit — his stage and area are on file. Notes saved against each.

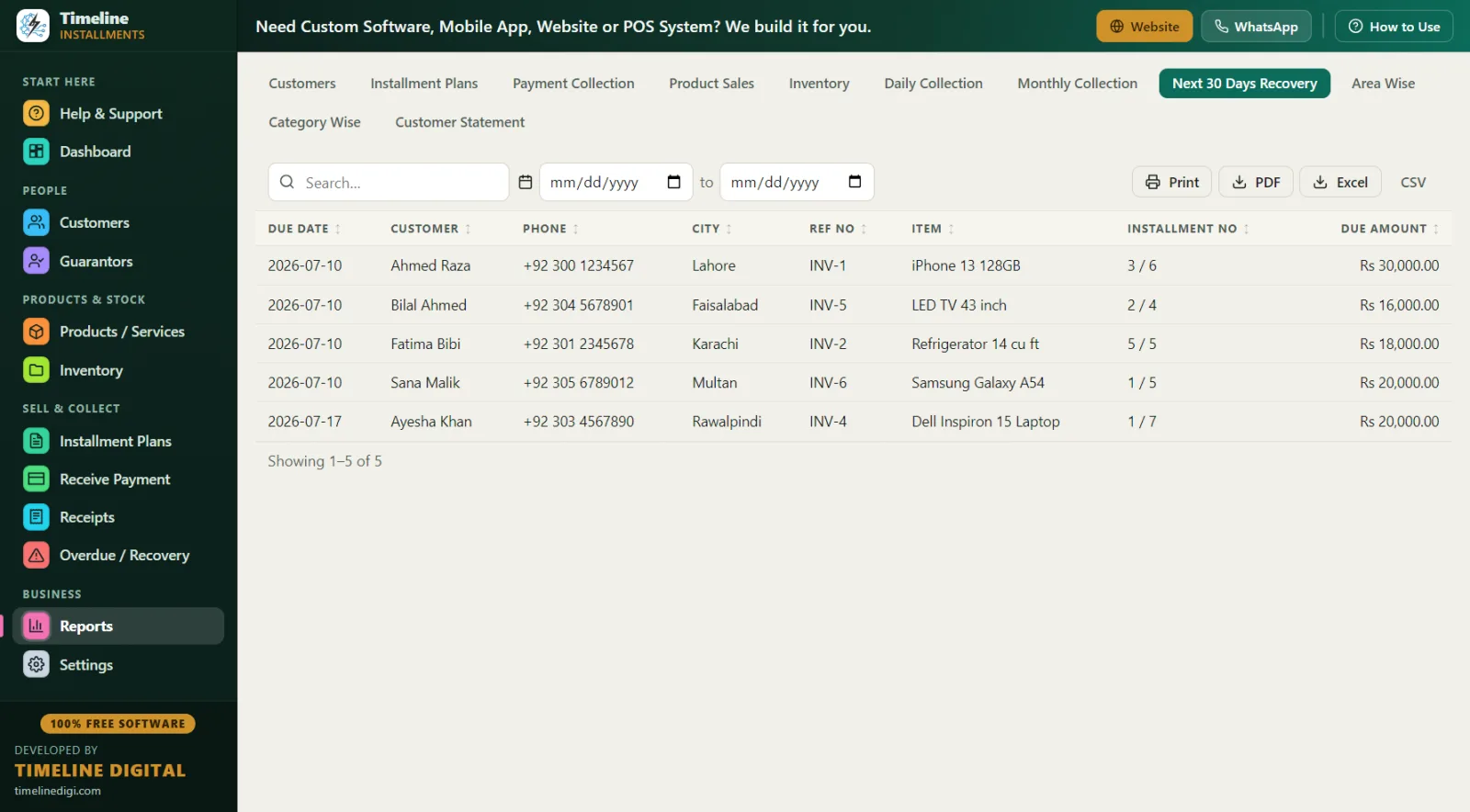

5:30 pm — Run Next 30 Days Recovery (due date, customer, phone, city, ref, item, amount) and forward reminders on WhatsApp for the week ahead. One-click Backup to the flash drive, close.

Free offline software vs subscription-based cloud systems

| Timeline Free Installment Manager | Typical subscription-based cloud system | |

|---|---|---|

| Price | ₦0 / KSh 0 / ₵0 — free forever | Monthly fees, often in USD |

| Internet needed | No — fully offline | Yes, constantly |

| Data bundles consumed | None | Ongoing |

| Data location | Your shop PC | Provider's servers abroad |

| Login / account | None | Required |

| Guarantor tracking | Built in, per plan | Varies |

| Daily/weekly/monthly plans | All three | Varies |

| Multi-branch, mobile apps | No (single PC) | Sometimes, at higher tiers |

Why free? Timeline Digital (timelinedigi.com) makes its money building custom software — cloud, mobile apps, multi-branch, POS. If your business grows into a fleet-financing operation with branches in three cities, that's a custom project; the free product stays free for everyone else.

Best practices for hire purchase in Nigeria, Kenya and Ghana

- Deposit first, always. 25–30% down (₦400,000 on a ₦1.4M okada) is the single best filter for serious buyers — and it's auto-receipted as payment one.

- Two guarantors on motorcycles. Family plus a community figure (stage chairman, association head). Record phone and ID for both.

- Verify the ID physically. NIN, Ghana Card, National ID or licence — see the card, enter the number.

- Match frequency to income. Riders earn daily — collect weekly. Salaried customers — monthly, dated after payday. The live schedule preview confirms dates before you save.

- Receipt every payment, even partial ones. The printed "Installments Paid X of Y" and remaining balance end most arguments.

- Remind before due dates. Run Next 30 Days Recovery weekly and send WhatsApp reminders two days ahead. Recovery is cheaper than repossession.

- Use late fees carefully. Fixed or percentage-of-balance per plan — set it, but waive for good customers who communicate.

- Back up weekly to a flash drive kept at home. One click, with reminders. Practise first in Sample Data mode with the 6-step quick start.