The fastest way to reduce late installment payments is to prevent them at the sale (real down payment, verified guarantor, signed schedule) and then follow up on day 1 late — not day 30 — working from a daily overdue list instead of memory. Shops that do these two things consistently keep overdue amounts a fraction of what "chase when it gets bad" shops carry.

Profit in the installment business isn't made at the sale — it's made at collection. A phone sold at a 20% markup that never gets collected isn't a sale; it's a donation with paperwork. This guide covers the nine tactics disciplined shops use, split into prevention (before the sale) and systematic collection (after), plus the escalation ladder, common mistakes, and a daily routine you can copy tomorrow.

Why do installment customers pay late?

Most installment customers pay late because they've learned that nothing happens when they do — not because they can't pay. There are three broad types of late payer, and each needs different handling:

| Type | Who they are | What works |

|---|---|---|

| Forgetful | Genuinely busy; money exists | A reminder call the day it's late. Pays within days. |

| Tester | Paying whoever chases hardest this month | Consistent day-1 follow-up. You must be the creditor who always calls. |

| Distressed | Real problem — job loss, illness | Restructure: partial payments, adjusted dates. Pressure alone fails here. |

| Never-intended | Planned to default from day one | Only prevention works: down payment, guarantor, ID. Filter them out at the sale. |

Notice that three of the four types are handled by systems — reminders, consistency, and screening — not by aggression. That's the theme of everything below.

How do you prevent late payments before the sale?

You prevent late payments by making every customer pass four gates before the product leaves the shop. Prevention beats recovery every single time.

1. Take a real down payment. 15–25% minimum. A customer with their own money in the deal protects the deal. Illustrative example: on a Rs 219,000 six-month phone plan, a Rs 39,000 down payment means the customer loses real money by walking away — and you've recovered part of your cost on day one. Down-payment resistance is itself a screening signal: the customers who fight hardest against putting money down are disproportionately the ones who would have defaulted. (How to build that pricing in the first place: calculate your installment price.)

2. Require a guarantor with a verified phone. Then — this is the step most shops skip — call the guarantor once at sale time: "Salaam, just confirming you're guaranteeing Ahmed's phone plan with us." Thirty seconds. Now the guarantee is real, the number is verified, and the guarantor knows they're on record. A guarantor who was never contacted at the sale will claim they never agreed when you call six months later.

3. Collect ID copy + photo + address. Recovery starts with being findable. CNIC/ID copy, a photo of the customer, and a home address you could actually visit. In Timeline Free Installment Manager, every customer record has a CNIC/ID field, an optional photo, and linked guarantors — so this isn't extra paperwork, it's just filling the form.

4. Print the schedule and have it signed. Exact dates, exact amounts, signatures. "I thought it was next month" dies when the customer holds a signed copy of the schedule. Timeline generates the full schedule with a live preview at plan creation; pair it with a proper installment agreement and you've closed the paperwork gap completely.

How do you collect systematically after the sale?

You collect systematically by working from a live list every morning, calling on the first late day, escalating in fixed steps, and recording everything — including partial payments.

5. Call on day 1 late — not day 30. The first late payment is a test, whether the customer knows it or not. A same-week call — polite, short, factual — signals that you track everything: "Salaam, this is [shop]. Your installment of 30,000 was due yesterday — when can we expect it?" Every week of silence teaches the customer that late is fine, and each of those lessons compounds. The shop that calls on day 1 gets paid before the shop that calls on day 20, out of the same customer's same limited money.

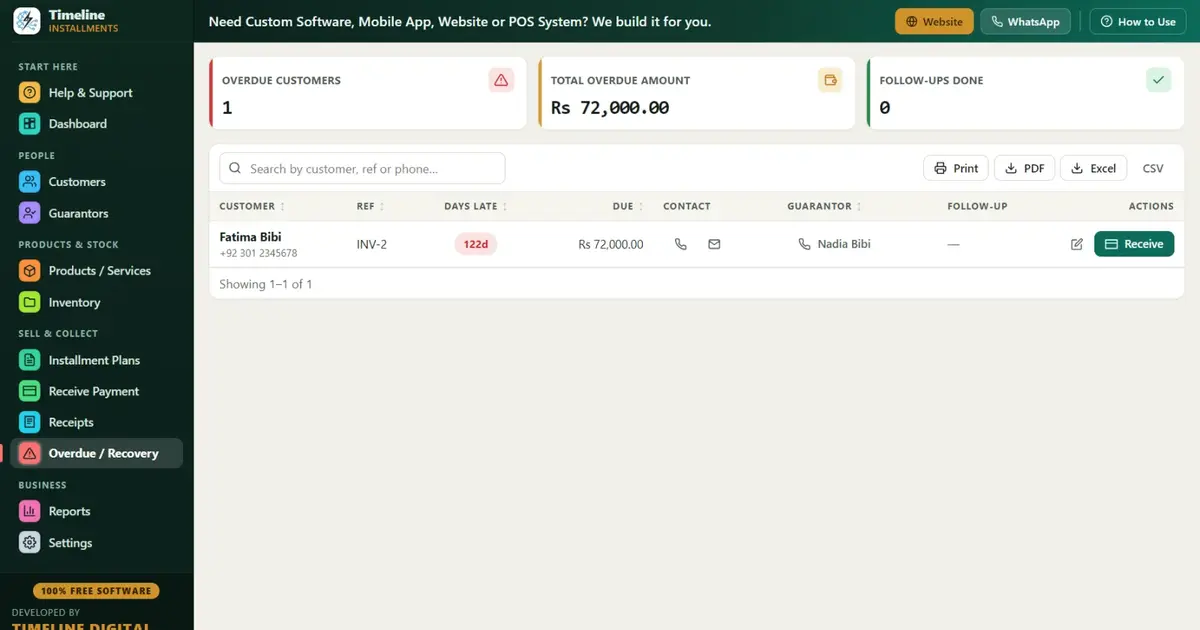

6. Work from a list, not memory. Every morning, open your overdue list: who, how many days late, how much, and the phone number. Memory-based recovery collapses past 20 customers; list-based recovery scales forever. Timeline's Overdue screen shows exactly this on one screen — days late, amount, customer phone, and the guarantor's contact right next to it for step two.

7. Plan the month ahead. Recovery isn't only chasing the late — it's landing the on-time. Print the Next 30 Days Recovery report: every upcoming installment with customer, phone, area, and amount. Hand it to your recovery person as a ready-made visit route, grouped by area so one trip covers a neighborhood. (It exports to PDF/Excel/CSV like all 11 of Timeline's reports; the Area Wise report also tells you which neighborhood carries the most exposure before you sell more there.)

8. Escalate in steps — the same steps, every time.

- Day 1–3 late: friendly reminder call to the customer.

- Day 7: second call + message. Ask for a specific date, and write it down.

- Day 10–14: call the guarantor. Calm and factual: "Ahmed's installment is two weeks late — can you help us reach him?" Most cases resolve here; social pressure from a guarantor works better than ten calls from you.

- Day 21: home or shop visit. Bring the printed customer statement showing exactly what's owed.

- Day 30+: final notice referencing the signed agreement, and a permanent stop on new plans for this customer.

Consistency matters far more than aggression. A predictable, polite ladder that always runs beats occasional angry outbursts — and keeps customers who were merely "testers" as future buyers.

9. Take partial payments — and record them precisely. 4,500 today beats 5,000 never. A customer paying something is maintaining the habit and the relationship; a customer told "full amount or nothing" often chooses nothing. The trap is recording: a partial scribbled as "paid" in a register loses the difference forever. Timeline applies partial payments to the oldest unpaid installment first, automatically, and the next printed receipt shows the true remaining balance and "Installments Paid X of Y" — so partials never turn into leakage. Settlement discounts count toward closing the plan too, so a negotiated early payoff closes cleanly on paper.

What does a daily recovery routine look like?

A working recovery routine takes about 10 minutes a day plus one weekly planning session:

| When | Action | Time |

|---|---|---|

| Every morning | Open Overdue screen; call every new day-1 late customer | 10 min |

| Every morning | Note promised payment dates from yesterday's calls; chase broken promises first | 2 min |

| Weekly (e.g., Monday) | Print Next 30 Days Recovery report; plan visits by area | 15 min |

| Weekly | Move day-10+ cases to guarantor calls | 10 min |

| Month-end | Run Customer Statement report; stop-list anyone 2+ installments behind | 15 min |

Shops that keep overdue low share one habit: recovery is a short daily routine driven by a live list, not a monthly panic driven by a register. The panic version always starts too late, hits too hard, and burns customers the routine version would have kept.

What are the most common recovery mistakes?

- Waiting for the amount to "become worth chasing." By the time three installments have piled up, the customer owes more than they can pay at once, and shame keeps them away from your shop entirely. Small and early beats big and late.

- Skipping the guarantor confirmation call at sale time. An unverified guarantor is a name, not a guarantee. Thirty seconds at the sale saves the whole tool from being useless later.

- Refusing partial payments. "Full amount only" sounds firm but converts slow payers into non-payers. Take the partial, record it exactly, print the receipt showing the new balance.

- Threatening on the first call. Aggression on day 1 burns forgetful customers — your best repeat buyers — to catch testers who would have responded to a polite call anyway. Save weight for the later rungs of the ladder.

- Selling a second plan while the first is late. The single most expensive mistake in this business. No exceptions — not for relatives, not for good history, not for "he's about to clear it."

- No paper trail on promises. "He said next Tuesday" must be written down and chased on Wednesday. Broken promises left unchased teach customers that promises to you are free.

- Chasing without receipts to show. Walking into a dispute without a printed statement turns a fact into an argument. Bring the customer statement; disputes end where documents begin.

Set up the system, free

Every tactic above runs on one thing: knowing exactly who owes what, today, with contact details one glance away. That's a software problem, and the software is free. Download Timeline Free Installment Manager — overdue tracking, guarantor contacts, the Next 30 Days Recovery report, and branded receipts, all offline on your own PC with no signup. Load the sample data, run tomorrow morning's 10-minute routine on it, and see how a live list changes the game. New to the business? Start with the full playbook: how to start an installment business.