To start an installment business in Pakistan or India, you need four things: enough capital for 15–25 active plans, a fixed set of rules for every sale (down payment, guarantor, ID, signed schedule), a record-keeping system that tracks every due date, and a daily collection routine. The model is simple — sell products at a marked-up "installment price" paid monthly — and the profit or loss is decided almost entirely by discipline, not by sales talent.

Selling mobiles, appliances, furniture, or motorcycles on installments (qist/کسٹ in Pakistan, EMI/kisht in India, kisti across South Asia) is one of the highest-margin retail models in the region — when collections are disciplined. When they're not, it's one of the fastest ways to turn working capital into a list of names who don't answer the phone. This guide is the practical playbook: the economics with real numbers, the setup, the rules, the paperwork, the software, and the collection routine that keeps default low.

How does the installment business model actually work?

The installment business works by selling a product at a higher "installment price" than the cash price, collecting a down payment on day one, and collecting the rest in fixed monthly amounts. You are making a credit sale, not giving a loan — you set one total price for deferred payment, and the customer agrees to a schedule.

Here's an illustrative example, using a phone in Pakistan:

| Item | Amount (example) |

|---|---|

| Cash price (your cost basis for the deal) | Rs 180,000 |

| Installment price (6 months) | Rs 219,000 |

| Markup | Rs 39,000 (~22%) |

| Down payment (day of sale) | Rs 39,000 |

| Amount financed | Rs 180,000 |

| Monthly installment × 6 | Rs 30,000 |

Notice the structure: the down payment equals your markup, so from day one your remaining exposure is the cash price — and every monthly payment after that reduces risk while the profit is already partly banked. Typical markups in the market run 20–35% over cash price for 6–12 month terms; shorter terms take less markup, longer terms and riskier customers take more. The full math, including how to keep monthly amounts round, is in our guide on calculating an installment price.

Two things kill this model, and both are record-keeping failures before they're customer failures:

- Default — customers who stop paying. Mostly preventable at the sale (down payment, guarantor, ID) and recoverable early (day-1 follow-up).

- Untracked partials and leakage — payments taken but recorded wrong, discounts nobody wrote down, due dates nobody chased. This one is invisible until you count.

How much capital do you need to start?

You need enough capital to fund 15–25 active plans in your product category — because the money comes back monthly, capital compounds, and a small disciplined start outperforms a big sloppy one.

Illustrative example for a mobile-focused shop: if your average phone costs Rs 60,000–180,000 wholesale and you target 20 active plans, you're looking at roughly Rs 1.5–3 million in stock capital, partially offset by down payments coming in immediately. A furniture or appliance seller can start lower; a motorcycle dealer needs more per unit but fewer units.

The compounding is the point. With 20 plans averaging Rs 25,000/month each, roughly Rs 500,000 flows back monthly — which funds 3–6 new phones, which become new plans, which increase next month's inflow. A shop that starts with 15 disciplined plans and reinvests collections typically outgrows a shop that started with 50 loose ones, because the loose shop's capital is stuck in overdue accounts.

Practical starting rules:

- Start in one product category you know — the one where you can judge resale value and spot a customer who's overpaying for status versus buying within means.

- Keep 2–3 months of shop expenses aside — rent and salaries can't wait for collections.

- Don't finance your stock on credit you can't service if collections run slow in month one. Slow first months are normal.

What rules should you never break on a sale?

Every plan must pass four gates — no exceptions for friends, relatives, or "known" customers:

- Minimum 15–20% down payment. The customer's own money in the deal is your best default insurance, and resistance to a down payment is itself a warning sign.

- A guarantor with a verified phone. Call the guarantor at sale time — 30 seconds — to confirm they're guaranteeing the plan. An unverified guarantor is decoration.

- ID/CNIC copy + photo + address. You must be able to find the customer. In Pakistan that's the CNIC; in India, Aadhaar or another government ID.

- Signed agreement + printed schedule. Exact dates, exact amounts, signatures from customer and guarantor. Use a proper installment agreement format — it turns future disputes into paperwork checks.

And one standing rule after the sale: no second plan while the first is late. Ever. The customer who wants a second phone while owing on the first is asking you to double a bad bet.

How should you price and market installment plans?

Price by working backward from a round monthly amount, and market the monthly number — never the "interest."

- Price = cash price + markup for the term. Then round so both the total and the per-month figure are clean: customers think per-month, so "Rs 30,000 monthly" sells better than "Rs 29,167 monthly" even at a similar total.

- Advertise the installment price and the monthly amount, not an interest rate. "Rs 39,000 down, Rs 30,000 × 6 months" is clear, honest, and culturally/religiously cleaner in both Pakistan and India — it's a credit sale at a stated price, not a loan with interest.

- Longer terms need bigger markups and better screening. A 12-month plan gives the world twelve chances to change; price for it and reserve it for customers with strong guarantors.

- Let the down payment flex, not the rules. A stronger customer can get a slightly better price; nobody gets to skip the down payment, guarantor, or paperwork.

What paperwork and records does each sale need?

Each sale needs one agreement file and a live payment record. The agreement file (paper) holds: the signed agreement, the printed schedule, the CNIC/ID copy, the customer photo, and the guarantor's details and ID. The payment record (software) tracks every payment against every due date.

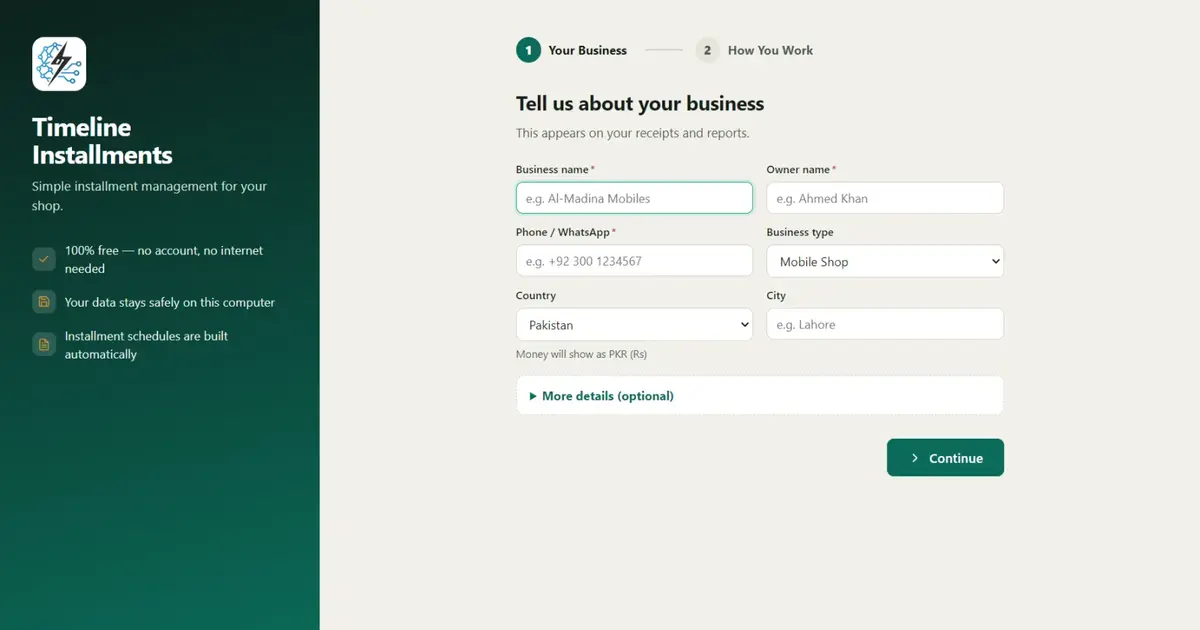

A paper register works until about 20 customers. After that, you need automatic schedules, receipts, an overdue list, and reports — and this is exactly where most new installment businesses quietly fail. Use Timeline Free Installment Manager, free offline Windows software built for this business:

- Currency auto-sets to PKR (Rs) in Pakistan or INR (₹) in India (150+ countries supported) — no configuration.

- CNIC/ID field and optional photo on every customer, with guarantors linked to every plan, and an inline "New Customer" button inside plan creation so a walk-in sale is one screen.

- Auto-generated schedules — monthly, weekly, or daily — with a live preview; the down payment records automatically as the first payment; late fees can be fixed or a % of the remaining balance.

- Branded receipts (print or PDF on any Windows printer) with your logo, remaining balance, "Installments Paid X of Y," and signature lines — print two per payment, one for the customer, one for the file.

- Partial payments apply oldest-first automatically, and settlement discounts count toward closing the plan.

- Product catalog with stock that auto-reduces on installment sales, plus low-stock alerts.

- Overdue screen (days late, amount, customer phone, guarantor contact) and 11 reports — including Next 30 Days Recovery, Area Wise, Category Wise, and Customer Statement — all exportable to Print/PDF/Excel/CSV.

- One-click Backup & Restore with reminders, sample data for practice, and an in-app 6-step quick start.

It's free forever, with no account or login and nothing uploaded — the developer, Timeline Digital, earns from paid custom builds, not from the app. Country-specific detail: installment software for Pakistan · EMI software for India · mobile shop installment software.

What collection routine keeps default low?

The routine that keeps default low is short, daily, and list-driven — about 10 minutes each morning plus a weekly planning session:

- Every morning: open the Dashboard → check Today's Due and the Overdue screen.

- Same day: call every customer who went late yesterday. Day-1 calls are the single highest-return habit in this business.

- Weekly: print the Next 30 Days Recovery report — every upcoming installment with customer, phone, area, and amount — and run visits by area. Move day-10+ cases to guarantor calls.

- Month-end: run the Customer Statement report; stop-list anyone 2+ installments behind, and check the Area Wise report to see which mohalla/colony carries the most exposure before selling more there.

The full escalation ladder — reminder call → guarantor call → visit → final notice — is covered step by step in our installment recovery tips. The short version: consistency beats aggression, partial payments beat standoffs, and everything gets written down.

What are the most common mistakes new installment businesses make?

- Selling to volume instead of quality in month one. Twenty carefully screened plans beat fifty loose ones — the loose fifty will eat your capital and your evenings.

- Waiving the down payment to close a sale. The waived down payment is usually the future default. The customer who can't produce 15% today won't produce 100% over six months.

- Skipping the guarantor call at sale time. An unverified guarantor claims ignorance later. Thirty seconds at the sale keeps the tool sharp.

- Running on a register past 20 customers. Due dates slip, partials get rounded to "paid," totals become unknowable. The failure is silent until money is missing.

- Chasing late payments monthly instead of daily. By day 30 the customer owes too much to pay at once and too much shame to visit your shop. Day-1 calls keep amounts small and relationships intact.

- Not recording discounts and partials precisely. "Pay 25,000 and we're settled" is fine business — if it's recorded as a settlement discount so the plan actually closes in the books.

- Growing area exposure blindly. If one neighborhood already owes you disproportionately, pause selling there until it collects down. The Area Wise report exists for exactly this.

- No backup. Your receivables list is the business. One click weekly to a USB drive.

How do you scale beyond one counter?

Scale in this order: recovery help first, then stock depth, then a second branch — and upgrade the software only when the operation genuinely outgrows one PC.

- At ~50–100 active plans: hire a recovery person, paid partly per successful collection, and hand them the printed Next 30 Days Recovery report as their route sheet.

- At 100+ plans: deepen stock in your best-collecting categories (the Category Wise report shows which), and formalize the stop-list policy.

- When you need multi-branch, cloud access, or a mobile app: the same developers behind the free app — Timeline Digital (WhatsApp +92 344 9310484) — build paid custom versions (mobile apps, cloud, multi-branch) on top of the system you're already running, so scaling doesn't mean starting over.

Step one is free

The installment business rewards exactly one thing: discipline, applied daily, to good records. The rules cost nothing, the routine costs 10 minutes a morning, and the software costs nothing at all. Download Timeline Free Installment Manager — free forever, offline, no signup — load its sample data to practice tonight, and open your first real plan this week.