How hire purchase works for UK retailers is simple at its core: the customer pays a deposit, takes the goods home, pays fixed instalments, and only becomes the legal owner when the final payment clears. This plain-English guide to how hire purchase works for UK retailers walks through the maths, the deposit and late-fee decisions, the polite British way to chase payments, and the records you must keep — with a worked £1,200 sofa example you can copy for your own shop.

If you run a furniture store, an appliance shop, a phone shop, or any high-street business where a £400–£2,000 price tag makes customers hesitate, hire purchase (HP) can turn "I'll think about it" into a signed agreement and a weekly payment. Let's break it down.

What Is Hire Purchase, Exactly?

Hire purchase is an agreement where the customer hires the goods while paying instalments, and purchases them with the final payment. That word order matters. Until the last instalment is paid:

- You (the retailer) remain the legal owner of the goods.

- The customer has possession and use, but not ownership.

- Ownership passes to the customer only when the final payment (sometimes called the "option to purchase" fee) is made.

This is what makes HP different from a simple credit sale, where ownership passes on day one and you're left chasing an unsecured debt. With HP, the goods themselves are your security. That's why HP has been the backbone of British instalment retail — from sofas to sewing machines — for well over a century.

A typical HP agreement has four moving parts:

- Cash price — what the item costs if paid in full today.

- Deposit — paid upfront, usually 10–25% of the cash price.

- Instalments — fixed weekly or monthly payments over an agreed term.

- Total HP price — deposit plus all instalments, usually higher than the cash price to reflect the credit you're extending.

How Does HP Compare to Pay-Weekly and BNPL for a High-Street Retailer?

Retailers often lump these together, but they work very differently behind the till. Here's an honest comparison for a typical UK high-street shop:

| Feature | Hire Purchase (in-house) | Pay-Weekly (in-house credit sale) | BNPL (Klarna-style third party) |

|---|---|---|---|

| Who owns goods during term? | You, until final payment | Customer, from day one | Customer, from day one |

| Who takes the credit risk? | You | You | The BNPL provider |

| Who gets paid upfront? | Nobody — you collect over time | Nobody — you collect over time | You, minus a merchant fee (typically 2–8%) |

| Deposit required? | Yes, usually 10–25% | Your choice | Rarely |

| Your margin on the credit | You keep 100% of any HP uplift | You keep 100% | You give up the fee; no uplift |

| Customer relationship | Weekly contact, strong loyalty | Weekly contact, strong loyalty | Owned by the app, not you |

| Works for customers with thin credit files? | Yes — your judgement | Yes — your judgement | Often declined by the algorithm |

| Regulatory weight | Consumer credit rules apply — seek advice | Consumer credit rules apply — seek advice | Provider handles most of it |

| Admin burden | Yours — needs good records | Yours — needs good records | Minimal |

The pattern is clear. BNPL is easy but takes a slice of every sale and hands your customer relationship to an app. In-house HP and pay-weekly keep the margin and the relationship in your shop — but only if your record-keeping is solid. More on that below, and see our deeper comparison at /blog/daily-weekly-monthly-installments for choosing the right payment frequency.

What Does a Real HP Deal Look Like in Pounds?

Let's price a real example: a £1,200 sofa sold on hire purchase.

The structure:

- Cash price: £1,200

- Deposit: £200 (about 17%)

- Instalments: 20 weekly payments of £50

- Total instalments: 20 × £50 = £1,000

- Total HP price: £200 + £1,000 = £1,200

In this example the HP price equals the cash price — a "0% uplift" deal some retailers use as a promotion. Many shops instead add an uplift for the credit. Here's how both versions compare:

| Line item | 0% uplift deal | 10% uplift deal |

|---|---|---|

| Cash price | £1,200 | £1,200 |

| HP price | £1,200 | £1,320 |

| Deposit (paid day one) | £200 | £200 |

| Balance to collect | £1,000 | £1,120 |

| Weekly instalment (20 weeks) | £50.00 | £56.00 |

| Your gross uplift | £0 | £120 |

| Weeks until you break even on a £700 cost price | Week 10 | Week 9 |

Two things to notice. First, with a £200 deposit and £50 a week, you've recovered a £700 wholesale cost by week 10 — everything after that is margin. Second, the deposit does real work: it filters out non-serious buyers and cuts your exposure from day one. For a full method on setting instalment prices, read /blog/calculate-installment-price.

If you track this in Timeline Free Installment Manager, the deposit is automatically recorded as the first payment with a printed receipt, and the app builds the 20-week schedule with a live preview before you save — so the customer sees exactly what "£50 every Friday for 20 weeks" looks like before signing.

How Should You Set Your Deposit and Late-Fee Policy?

A written policy protects you and keeps every staff member consistent. Here's a sensible starting framework for a UK high-street shop:

Deposits:

- Standard: 15–20% of the HP price. Below 10%, you attract buyers with no real commitment. Above 25%, you lose sales to BNPL.

- New customers: lean higher (20%+). Repeat customers with a clean record: you can go lower.

- Never waive the deposit entirely on a first agreement. The deposit is your first test of whether the customer can actually save and pay.

Late fees:

- Decide between a fixed fee (e.g. £5 per missed week) or a percentage of the remaining balance (e.g. 2%). Fixed fees are easier to explain over the counter; percentage fees scale with larger balances.

- Whatever you choose, it must be stated in the signed agreement — never sprung on the customer later. Get a template at /blog/installment-agreement-format.

- Keep it proportionate. A punitive fee damages goodwill and may cause problems under consumer credit rules.

- Timeline supports both models — fixed or % of remaining balance — so the fee calculates itself instead of being argued about at the counter.

Grace periods: many British retailers quietly allow 2–3 days before a late fee applies. Life happens; a bin-day payment that arrives Monday instead of Friday is not a crisis. Put the grace period in writing too.

What About the FCA and Consumer Credit Rules?

Here is the awareness paragraph every UK retailer needs — and please treat it as awareness only, not legal advice. In the UK, hire purchase agreements with consumers generally fall under consumer credit regulation overseen by the Financial Conduct Authority (FCA), and offering regulated credit typically requires the right authorisation or an exempt structure. The rules cover things like how agreements are documented, what customers must be told, and how arrears are handled. Before you offer HP to the public, consult a solicitor or a consumer-credit compliance professional about your specific setup. Software like Timeline Free Installment Manager is a record-keeping tool — it tracks agreements, payments, and balances accurately, but it does not make your business compliant and is not a substitute for professional advice.

How Do You Chase Late Payments — Politely and Effectively?

British collections work best when they are firm, early, and unfailingly polite. A cadence that works for hundreds of pay-weekly shops:

| Days late | Action | Tone |

|---|---|---|

| 1–2 days | Nothing, or a friendly text: "Hi Sarah, just a reminder your £50 was due Friday — pop in when you can." | Light |

| 3–5 days | Phone call. Ask if everything's alright before asking for money. | Warm, human |

| 7 days | Second call plus the late fee applied (per the signed agreement). Offer a catch-up plan. | Firm but kind |

| 14 days | Letter or formal text stating the arrears figure and next steps in the agreement. | Formal |

| 21+ days | Follow the remedies in your agreement — with professional advice, since consumer credit rules govern repossession and default. | Procedural |

The single biggest predictor of recovery is speed. A payment chased on day 2 gets paid; a payment ignored for three weeks becomes a habit. Timeline's Overdue screen lists every late plan with days late, amount owed, and phone numbers (including the guarantor's), so Monday morning collections take ten minutes, not an hour. Its Next 30 Days Recovery report tells you exactly what cash should arrive this month. For more tactics, see /blog/installment-recovery-tips.

What Records Must You Keep — and Can Free Software Do It?

An HP business lives or dies on its records. At minimum, keep:

- The signed agreement — cash price, HP price, deposit, schedule, late-fee terms, signatures.

- Customer identity — name, address, phone, and an ID reference.

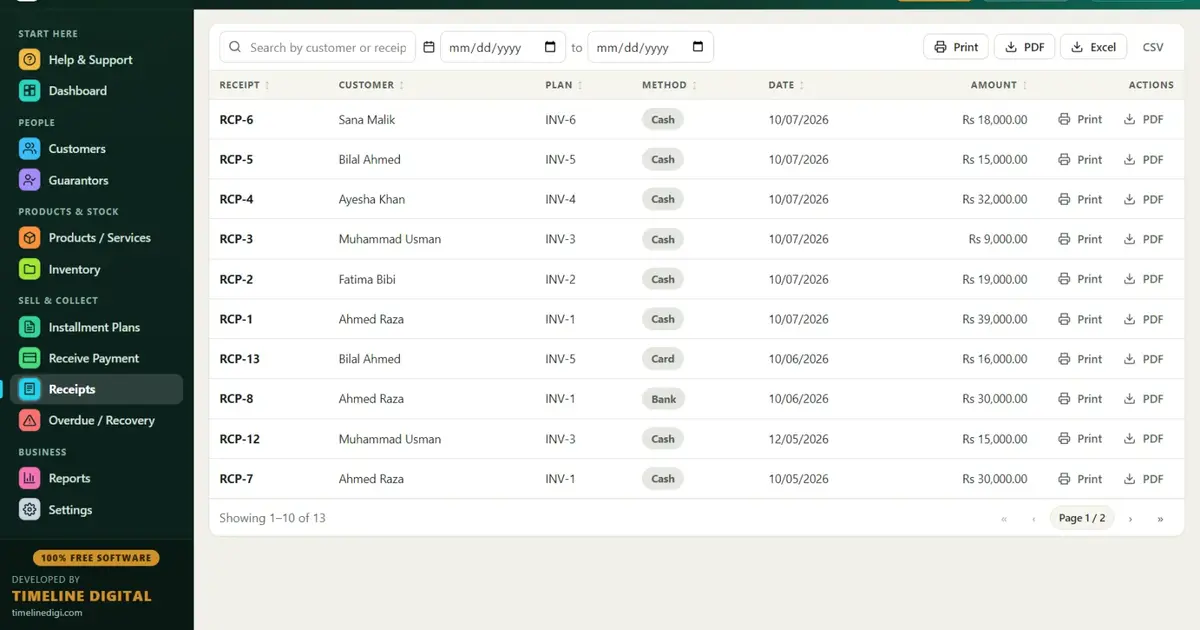

- Every payment — date, amount, method, and a receipt for the customer.

- The running balance — what's left, updated the moment money changes hands.

- Arrears history — what was late, when, and what you did about it.

You can do this in a ledger book, but one spilled tea or one lost page and you're relying on memory against a customer's word. A spreadsheet is better, but formulas break and nobody prints receipts from Excel at the counter.

Timeline Free Installment Manager (v1.6.0, by Timeline Digital) was built for exactly this job, and it's 100% free forever — Timeline Digital sells custom software, and this app is how they introduce themselves. For a UK shop it means:

- Runs on Windows 10/11 (about 90 MB), no account or login, and the database is fully offline — customer data stays on the shop PC, never in someone's cloud.

- Currency sets itself to £ automatically from your country.

- Auto-generated weekly schedules with a live preview — the £1,200 sofa deal above takes under a minute to set up.

- Deposit recorded automatically as the first payment, with a printed receipt on the spot.

- Branded receipts (print or PDF) showing your logo, "Installments Paid X of Y", the remaining balance, signature lines, and an editable terms footer.

- Late fees as fixed or % of remaining balance; partial payments applied oldest-first; discounts count toward settlement.

- Customer records with an ID field and guarantors linked to plans; stock auto-reduces when you sell on a plan.

- 11 reports — including Daily Collection, Customer Statement, Area Wise, and Next 30 Days Recovery — exportable to Print, PDF, Excel, or CSV.

- One-click Backup & Restore, plus a Sample Data practice mode so you can learn it without touching real accounts.

See the UK page at /hire-purchase-software-uk or the overview at /free-installment-management-software.

---

Ready to put your HP book in order? Download Timeline Free Installment Manager — free forever, offline, and set up for £ from the first click. Try it with Sample Data before you enter a single real customer: /free-installment-management-software.