To run a Christmas layaway program, launch it in September or October, take a 10-20% deposit to reserve the item, collect weekly payments through the fall, and set a final pickup cutoff of December 15-20 so every gift is paid off and out the door before Christmas. A well-run Christmas layaway program turns holiday browsers into committed buyers months before the December rush — the customer locks in the gift, you lock in the sale, and the deposit makes it real.

This playbook gives you the full timeline, the exact policy decisions with recommended numbers, a worked dollar example, a staff script for the register, and the pitfalls that cost stores money every January.

Why Does Layaway Convert Holiday Browsers Into Buyers?

Every October, your store fills with people who have picked out exactly what they want to give — and can't pay for it in one visit. Without layaway, those shoppers do one of three things: put it on a card they'd rather not use, promise to "come back closer to Christmas" (and buy it somewhere else), or scale down to a cheaper gift. All three are losses for you.

Layaway captures them, and it works on two customer groups in particular:

- Budget shoppers. Families planning holiday spending across three months of paychecks. A $350 console is painful in one hit; $28 a week starting in October is a line item they can plan around. Layaway is how they buy the good gift instead of the compromise gift.

- No-credit customers. Shoppers without cards, with maxed cards, or who simply refuse to carry a holiday balance into January. Layaway needs no credit check, no approval, no interest — just a deposit and a schedule. For these customers, you're not competing with other stores; you're competing with "can't buy it at all."

And layaway has a quiet advantage over BNPL at holiday time: the customer doesn't take the item home until it's paid off. No debt hangover, no returns wave in January, and no default risk on merchandise that already left the store — if a plan is abandoned, you still have the item to restock and resell. (For year-round installment selling where the item leaves with the customer, see how BNPL compares to in-house installments.)

There's a bonus you'll feel in November: every layaway payment is a store visit, and layaway customers walk past your shelves every week for two months. Stocking-stuffer sales to layaway customers are real money.

When Should a Christmas Layaway Program Start and End?

The calendar is half the program. Here's the timeline that works for US retail:

| Date | Milestone |

|---|---|

| Early-to-mid September | Finalize your written policy, set up tracking, train staff on the script. |

| Late September - early October | Launch. Signage up, staff offering it at checkout. The earlier a customer starts, the smaller each payment — a September start on a $350 item means roughly $28/week; a November start means $70/week. |

| October - November | Peak sign-up season. Weekly payments flowing; run your overdue check every Monday. |

| Around Thanksgiving | Last comfortable start date for weekly plans. After this, plans get short and payments get big — it's fine to keep signing people up, but set expectations. |

| December 15-20 | Final payment and pickup cutoff. Every plan must be paid off and picked up by this date. Pick one day in that window, print it on every agreement, and hold it. |

| Late December | Contact anyone who missed the cutoff; apply your written cancellation policy to abandoned plans; restock unclaimed items while they can still sell at full price. |

Why is the December 15-20 cutoff sacred? Three reasons: customers need the gift before Christmas, not on the 24th at closing time; you need those final days for regular full-price holiday selling, not layaway pickups; and any item that isn't picked up still has a week of prime selling season left when you restock it. A cutoff of "sometime before Christmas" is how stores end up storing unclaimed merchandise into February.

What Should Your Layaway Policy Say? (Design Table)

Write the policy on one page, print it on every agreement, and apply it identically to every customer. Here are the decisions and the numbers that work:

| Policy decision | Recommended setting | Why |

|---|---|---|

| Deposit | 10-20% of the item price | Enough commitment to filter out impulse reservations; low enough that budget shoppers can start today. Use 20% on high-demand items you're pulling off the sales floor. |

| Payment cadence | Weekly (biweekly acceptable) — use weekly | Weekly matches paychecks, keeps each payment small, and surfaces a stalled plan in 7 days. A monthly holiday layaway only gets 2-3 payments before Christmas — one miss kills the plan. |

| Term length | Item paid in full by your pickup cutoff | Work backward from the cutoff: sign-up date to December 15-20 defines the number of payments. |

| Cancellation / restocking fee | A flat fee or small percentage, stated in writing, deducted from the refund | Covers your cost of holding the item off the floor. State rules on layaway fees and refunds vary — awareness only, confirm your numbers with a professional. |

| Price-adjustment policy | Price locked at sign-up; no adjustment if the item goes on sale later — say so in writing | This is the #1 December argument at the register. Decide it in September, print it on the agreement, and the argument never happens. |

| Missed-payment rule | Grace period (e.g., 7 days), then contact; plan canceled per policy after X missed payments | Written and consistent — see pitfalls below. |

| Cutoff date | One specific date, December 15-20, on every agreement | See the timeline above. |

Every agreement should also include: item description, total price, deposit paid, each payment amount and due date, the customer's ID on file, and signature lines. Our installment agreement format guide maps the fields; the same skeleton works for layaway.

What Does a Real Christmas Layaway Look Like in Dollars?

Here's an example you can copy at the register.

The sale: On October 9, a customer wants a $350 game console for their kid's Christmas. You offer 20% down and weekly payments, paid off well before your December 18 pickup cutoff.

| Line item | Amount |

|---|---|

| Item price (locked at sign-up) | $350 |

| Deposit at checkout (20%) | $70 |

| Balance on layaway | $280 |

| Weekly payment (10 payments) | $28 |

| Final payment week | Mid-December, before the cutoff |

| Pickup date | December 18 |

| Interest or credit check | None |

| Total paid by customer | $350 |

Look at it from the customer's side: $28 a week is less than many families spend on a pizza night, and on December 18 they walk out with the exact console they chose in October — no card balance, no January bill. From your side: the sale was locked in 11 weeks before Christmas, the $70 deposit committed the customer, and if the plan had been abandoned, you'd still hold the console with a week of prime selling season left.

Record the $70 deposit as payment #1 and hand over a receipt showing "Paid 1 of 11 — remaining balance $280." That receipt is the customer's proof and your paper trail, and every weekly receipt after it counts down to pickup day.

What Should Staff Say to Offer Layaway at Checkout?

Layaway programs fail quietly when staff never mention them. Signage helps, but the offer at the register is what converts. Train every cashier on this script:

When a customer hesitates at a price, asks about holding an item, or says "I'll come back":

"We can put that on Christmas layaway for you today — you'd put down $70 now, then it's just $28 a week, and it's paid off and ready for pickup by December 18. That way it's reserved for you and nobody else can buy it. Want me to set that up? It takes about two minutes — I just need your ID and a phone number."

Why this wording works:

- It leads with the small numbers ($70 now, $28 a week), not the $350 total.

- "Reserved for you and nobody else can buy it" triggers the real holiday fear — the hot item selling out in December.

- It names the pickup date, which makes the plan feel finished, not open-ended.

- It ends with a low-effort close ("two minutes, ID and a phone number").

Two more staff rules: offer layaway to everyone who hesitates, not just customers who "look like" layaway customers — you cannot tell budget from browsing; and never negotiate policy at the register. The printed policy is the policy.

What Are the Common Layaway Pitfalls (and How Do You Avoid Them)?

Stores rarely lose money on layaway itself. They lose it on sloppy edges:

- No cutoff date. The classic. Plans with no printed final date drift into "I'll grab it after New Year's," and you're warehousing sold-but-unpaid inventory in January. Fix: one date, December 15-20, on every agreement, with a reminder call the week before.

- Verbal policies. A cashier "pretty sure" the deposit was refundable, a manager who waived a fee once — every unwritten rule becomes a December dispute. Fix: one printed policy on every agreement and every receipt, applied to everyone. If your receipts have an editable terms footer, put the policy there so the customer re-reads it at every payment.

- Unclaimed items. Some plans will be abandoned — customers move, budgets collapse. Without a written cancellation rule, that item sits in the back while the store argues with itself about refunds. Fix: written rule (refund minus the stated cancellation fee, item restocked after the cutoff), and make late-plan contact calls in early December while there's still time to finish or cancel cleanly.

- Memory-based tracking. Fifteen layaway plans tracked in a notebook means someone will miss a payment nobody notices until pickup day. Fix: software with a live overdue list — see below.

- Losing the deposit paper trail. Every payment, starting with the deposit, needs a receipt with a running balance. "I paid $28 two weeks ago" is unanswerable without one.

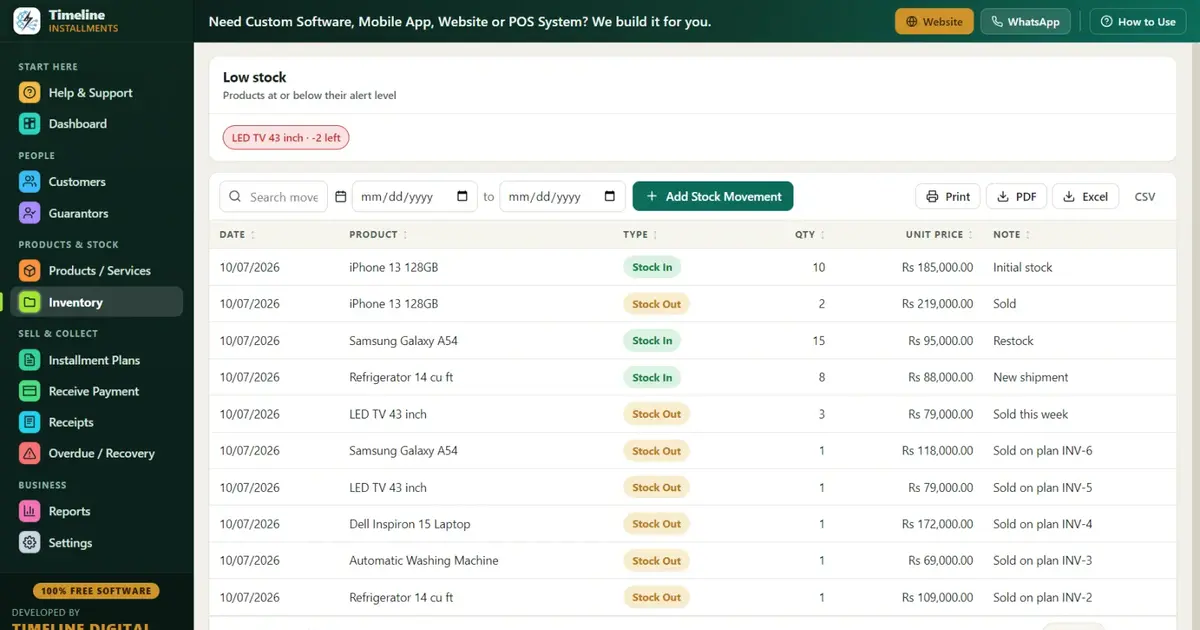

How Do You Track Layaway Schedules, Receipts, and Pickup Lists for Free?

A Christmas program means dozens of plans, each with its own schedule, all ending in the same two-week window. That's exactly the workload to hand to software — and it doesn't have to cost anything.

Timeline Free Installment Manager (v1.6.0, by Timeline Digital) is a free Windows 10/11 desktop app — 100% free forever, no trial and no catch; Timeline Digital sells custom software and this tool is their introduction. For a layaway program:

- Auto-generated weekly schedules with a live preview — enter the item, deposit, and weekly amount, and the customer sees every payment date through pickup before signing.

- The deposit is auto-recorded as payment #1 with a printed receipt at the register.

- Branded print/PDF receipts with your logo, "Installments Paid X of Y," the remaining balance, signature lines, and an editable terms footer — paste your layaway policy there so the cutoff date and cancellation rule ride on every receipt.

- Customer files with ID and references linked to each plan, so pickup day is a two-second identity check.

- An Overdue screen with days late and phone numbers — your Monday-morning call list through the fall.

- 11 reports including Next 30 Days Recovery (your December cash forecast), Customer Statement (the full history for any disputed plan), and Daily Collection — exportable to Print/PDF/Excel/CSV. Filter plans finishing by your cutoff and you have your pickup list.

- Partial payments post oldest-first and discounts count toward settlement — handy when you knock a little off to close out a plan before the cutoff.

- Fully offline with a local database, no account — customer data stays in the store. About a 90 MB install, USD auto-set for the US with MM/DD/YYYY dates, one-click Backup & Restore, and a Sample Data practice mode — perfect for training seasonal staff on fake plans before October.

There's a deeper walkthrough in our layaway software guide, and if plans stall in November, our installment recovery tips cover the calls that save them.

---

Planning your holiday season? Download Timeline Free Installment Manager now, build a few practice plans in Sample Data mode, and have your Christmas layaway program ready before the first October browser asks, "Can you hold this for me?" Stores that also sell on terms year-round should see our guides to in-house financing and rent-to-own payment tracking.